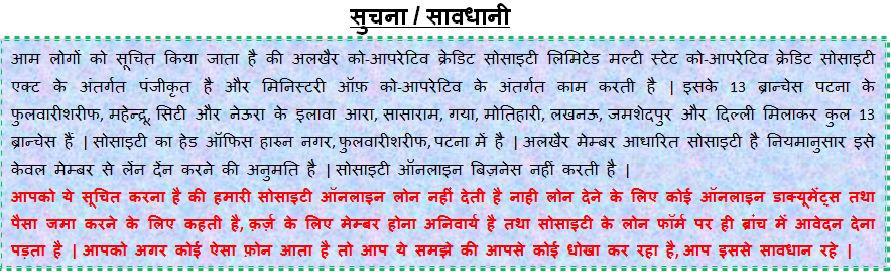

|

|

Co Operative: History, Status, Relevance 1. Background In India, the concept of cooperation is not new. It was embedded in our past as an economic forum of governance. It is visible in our philosophy and the Indian way of life Kautilya Arthashastra refers to cooperative as guilds of workmen who carry on any cooperative work, prescribing that they should divide their earnings equally or as agreed upon among themselves? The above is very relevant in the present day context of the non- agriculture cooperative credit societies(NACCS). These are cooperative financial institutions, owned, controlled and for the members. The Non-Agricultural Cooperative Credit Societies (NACCS) play a prime place in crafting, Indian urban Poor?s economic development. In fact the cooperative system is one of the main pillars providing vital credit support to the lower middle class people and non- agricultural cooperative credit societies provide the necessary infrastructure. They promote and encourage thrift, self help and meet the financial requirements of their members. Their focus is on serving the people living in poverty. Most cooperatives are organized on the basis of profession. The cooperative credit society offers services to members from all walks of the society more than financial services. They provide a chance to their members to own their own financial institution and help them create opportunities such as starting their own business, build their house, education of their children etc. They play an important role in spreading ethical values and principles of cooperatives in the country. Near 5 crores members are benefited from 50,000 non- agricultural cooperative credit societies spread over the whole of the country. 2. Origin & Legal Status The policy response of the British Government to the problem of rural indebtness was to initiate the process of organization of cooperative societies as alternative institutions providing credit to the people. Taking clue from that and to provide institutional support to the urban poor some erstwhile organized cooperative credit societies in the urban areas. The first known mutual aided society is said to have been organized in 1889 in Baroda in Gujarat State under the name of Anyonya Sahakari Mandali which later became a bank. This movement of NACCSs has over 150 years of history. In Italy and German urban credit institutions were successfully running during the period 1855-1885. Up till 1904 in India, the cooperative credit societies were functioning without any statutory regulation. The first registered cooperative credit society was in Canjeevaram in Madras. It was only after the passing of the cooperative credit societies Act 1904 that legal status was conferred on credit societies. Subsequently, in 1905, the Betegiri Cooperative Credit Society in Dharwar district and Banglore City Cooperative Credit Society in Mysore State were registered. The scope of Cooperative Societies Act 1904 was restricted basically to regulate agriculture cooperative credit societies. But then with the passing of time, looking to the needs of the societies, institution of ?Registrar of Cooperative Societies? came into existence, with the passing of 1912 Cooperative Societies Act. In fact, this act served as a model for the subsequent acts passed by various state governments when ?cooperation? was made provincial subject in 1919. This act also gave the movement its size and shape and was a pace setter of cooperative activities and stressed the basic concept of thrift, self help and mutual aid. Different types of non-agricultural cooperative credit societies are working in India, in urban and semi urban areas. There are societies with general public as members and cooperative societies with employees of a particular organization are members either registered under the state cooperative societies act or under the Multi State cooperative societies Act, depending upon there area of operation. Some of the societies are registered under mutually aided or suharda act too. 3. Status of non-agricultural cooperative credit Societies as financial intermediaries All cooperatives are essentially self help groups. Like in other parts of the developing world, the financial sector in India also consists of two major parts, i.e. the formal financial sector and the informal financial sector. 4. Formal Financial Sector The formal financial sector comprises of a. The banking sector b. The non-banking financial organizations that are registered under a particular law and are supervised by a financial regulator like, NBFCs and cooperative societies. 1) Institutions under the banking sector are characterized by the fact that a. They are permitted to accept deposits from the public and open cheque operated accounts. b. They are members of the payment systems of the country, operating in the clearing house. These institutions are regulated by RBI under the Banking Regulations Act. II. Non-banking financial institutions are also regulated entities. Some of them are allowed to accept deposits from public under specific conditions and are regulated by RBI. They are however, not members of the payment system and are not allowed to maintain and operate cheque accounts. There are other entities that are not permitted to accept deposits from non-members, cooperative credit societies fall under such a category. These are permitted to accept deposits from their members only. They are also not admitted to clearing houses and are not members of the payment systems. However, due to historical developments, all banking and non-banking entities are not strictly differentiated as above. Earlier, all banks were joints stock companies that were governed by Banking Companies Act which later became Banking Regulation Act. From 1920?s large number of such banks were in operation and failures/ bankruptcies were common. In addition to these banks, a large number of cooperative credit societies that had, over the decades progressively grown in size and providing banking services came to be known as cooperative banks. Till 1976, they were registered only under the respective state cooperative societies acts and RBI had no control over them. When the BR Act was amended in1966 and such institutions calling themselves banks and doing banking business, were brought under the Act, it was necessary for the definitions of co-operative banks to be included in the BR Act. Therefore B.R. Act Section5(C) of Section 56(AACS) was amended to include definition of ?Cooperative Banks?, ?Cooperative Society? ?Primary Cooperative Bank? and ?Primary Agricultural Credit Society? The non-agricultural cooperative credit societies today fall under the definition of ?cooperative credit societies? and the ?Cooperative Banks? are defined as a ?state cooperative bank? a ?district central cooperative bank? and a ?primary cooperative bank?. While ?state cooperative bank and district central cooperative bank? are defined and explained in the NABARD Act, the ?primary cooperative banks? is defined as cooperative society other than a primary agricultural society. 5. Cooperative Credit Societies The definition of a ?Cooperative Credit Society? given in the Banking Regulation Act is as follows. ?cooperative credit society means a cooperative society, the primary object of which is to provide financial accommodation to its members and includes a land mortgage bank? 6. Status of Cooperative Credit Societies The cooperative credit societies do not come under the preview of Banking Regulation Act 1949 although they are defined as ?cooperative credit societies? in the Act. The Reserve Bank of India therefore, does not exercise any control over the working of these societies. The Registrar Cooperative Societies of the states under whose jurisdiction these non-agricultural cooperative credit societies? falls, is the authority for registering cooperative credit societies and to exercise control and supervision over the business of a non-agricultural cooperative credit society as per the provisions of the cooperative societies acts and rules. |

||||||||||||||

| Copyright ® 2011-12 Alkhair | Disclaimer | Sitemap | Feedback |